Research, News, and Market Data on ARLP

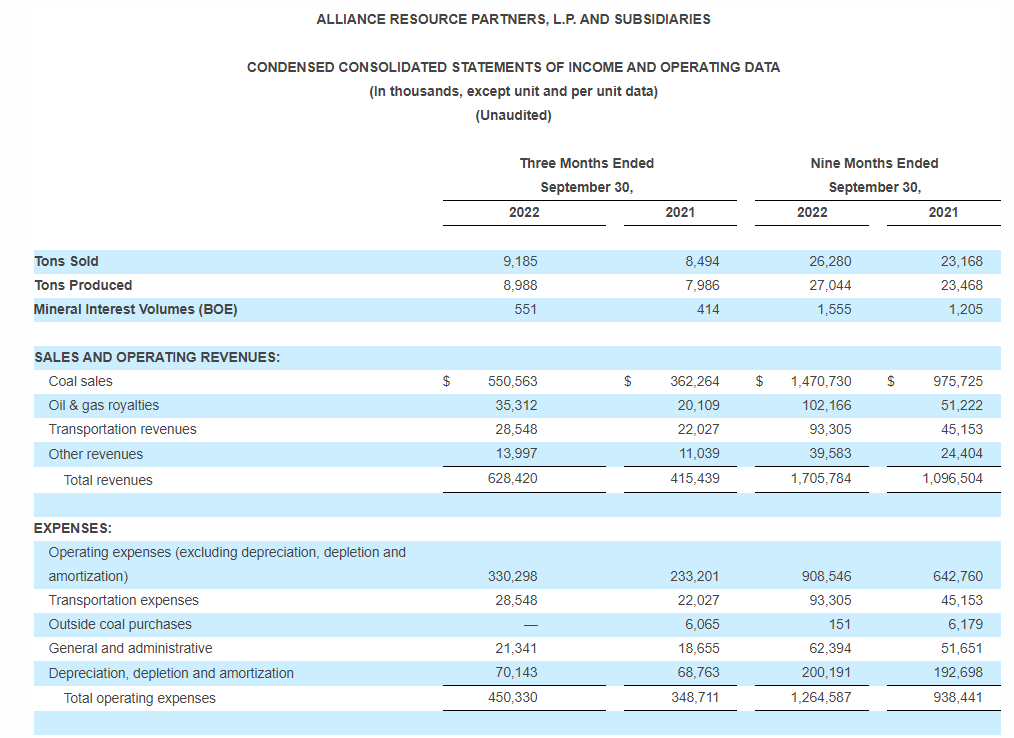

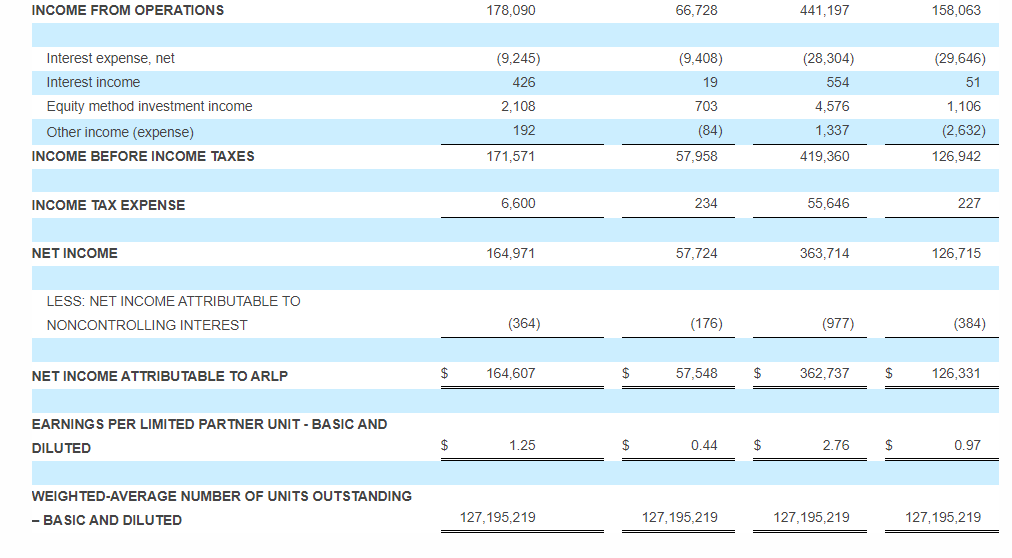

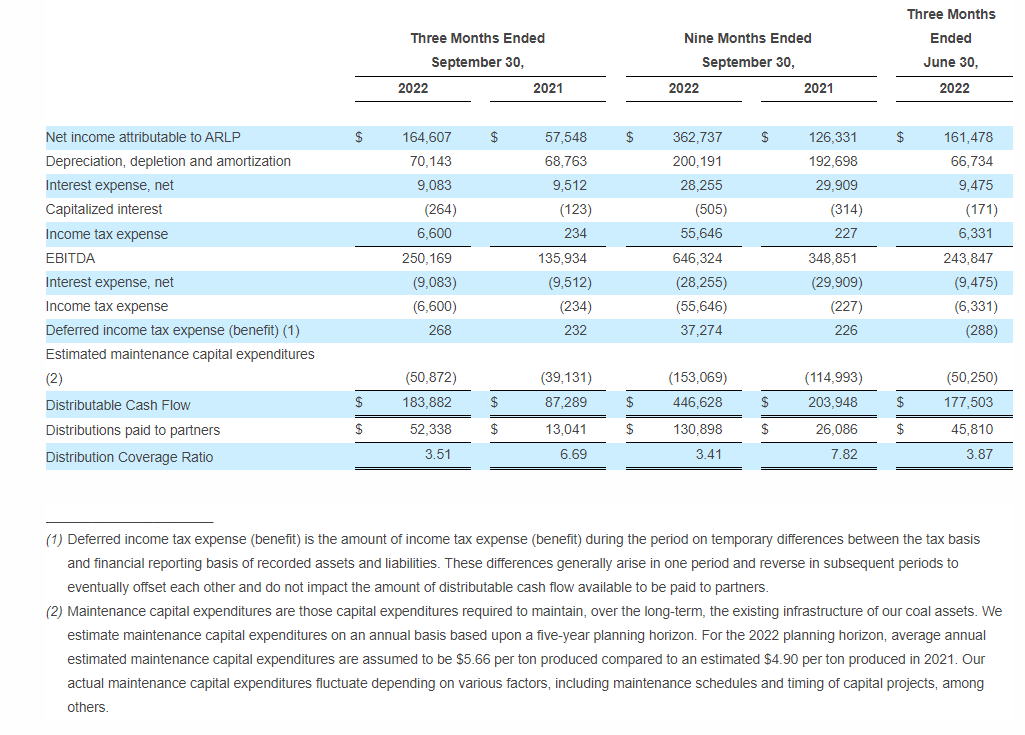

TULSA, Okla.–(BUSINESS WIRE)– Alliance Resource Partners, L.P. (NASDAQ: ARLP) today reported substantial increases to financial and operating results for the quarter ended September 30, 2022 (the “2022 Quarter”) compared to the quarter ended September 30, 2021 (the “2021 Quarter”). Total revenues in the 2022 Quarter increased 51.3% to a record $628.4 million compared to $415.4 million for the 2021 Quarter as a result of significantly higher coal sales revenues, which rose $188.3 million to $550.6 million, and oil & gas royalties revenues, which jumped 75.6% to $35.3 million. Coal sales revenues increased on the strength of record coal sales prices, which rose 40.5% in the 2022 Quarter to $59.94 per ton sold, and increased coal sales volumes, which were 8.1% higher compared to the 2021 Quarter. Oil & gas royalties revenue in the 2022 Quarter benefited from significantly higher volumes and sales price realizations per BOE, which increased 33.1% and 31.6%, respectively, compared to the 2021 Quarter. Total operating expenses increased to $450.3 million in the 2022 Quarter, compared to $348.7 million in the 2021 Quarter, due primarily to increased coal sales volumes and ongoing inflationary cost pressures. Net income for the 2022 Quarter increased 186.0% to $164.6 million, or $1.25 per basic and diluted limited partner unit, compared to $57.5 million, or $0.44 per basic and diluted limited partner unit, for the 2021 Quarter. EBITDA also increased 84.0% in the 2022 Quarter to $250.2 million compared to $135.9 million in the 2021 Quarter. (Unless otherwise noted, all references in the text of this release to “net income” refer to “net income attributable to ARLP.” For a definition of EBITDA and related reconciliation to its comparable GAAP financial measure throughout this release, please see the end of this release.)

Performance in the 2022 Quarter also improved compared to the quarter ended June 30, 2022 (the “Sequential Quarter”) as modest increases to coal sales volumes and pricing pushed both coal sales and total revenues higher by 3.5% and 1.9%, respectively. Increased revenues, partially offset by higher total operating expenses in the 2022 Quarter, led net income and EBITDA higher by 1.9% and 2.6%, respectively, both as compared to the Sequential Quarter.

Total revenues increased 55.6% to $1.71 billion for the nine months ended September 30, 2022 (the “2022 Period”), compared to $1.10 billion for the nine months ended September 30, 2021 (the “2021 Period”), primarily due to substantial increases in prices and volumes from both coal and oil & gas royalties. Higher revenues, partially offset by increased total operating and income tax expenses, led to significantly higher net income, which rose 187.1% to $362.7 million for the 2022 Period, or $2.76 per basic and diluted limited partner unit, compared to $126.3 million, or $0.97 per basic and diluted limited partner unit, for the 2021 Period. EBITDA increased 85.3% in the 2022 Period to $646.3 million compared to $348.9 million in the 2021 Period.

As previously announced on October 28, 2022, the Board of Directors of ARLP’s general partner (the “Board”) increased the cash distribution to unitholders for the 2022 Quarter to $0.50 per unit (an annualized rate of $2.00 per unit), payable on November 14, 2022, to all unitholders of record as of the close of trading on November 7, 2022. The announced distribution represents a 150.0% increase over the cash distribution of $0.20 per unit for the 2021 Quarter and a 25.0% increase over the cash distribution of $0.40 per unit for the Sequential Quarter.

“With energy market fundamentals remaining favorable during the 2022 Quarter, ARLP again delivered strong financial and operating performance, as we posted record quarterly total revenues and income from operations as well as significant increases to net income and EBITDA compared to the 2021 Quarter,” said Joseph W. Craft III, Chairman, President and Chief Executive Officer. “Higher coal sales and production volumes combined with record per ton price realizations drove our total Coal Segment Adjusted EBITDA up 77.8% to $224.6 million as margins per ton sold jumped $9.58 compared to the 2021 Quarter. Strong energy markets also continued to benefit our royalty businesses as increased volumes and commodity price realizations led to increased total royalty revenue and record Segment Adjusted EBITDA during the 2022 Quarter.”

Mr. Craft added, “ARLP was also able to execute new coal sales commitments for delivery of 5.6 million tons through 2025 at prices supporting higher margins in the future. With ARLP sold out for this year and solid contracted coal sales volumes in 2023 and 2024, we have good visibility into our ability to generate cash flow growth over the next several years. Reflecting our strong year-to-date performance and future expectations, ARLP’s Board elected to accelerate our previously planned increases to cash distributions to unitholders by declaring a $0.50 per unit distribution for the 2022 Quarter, as communicated last week.”

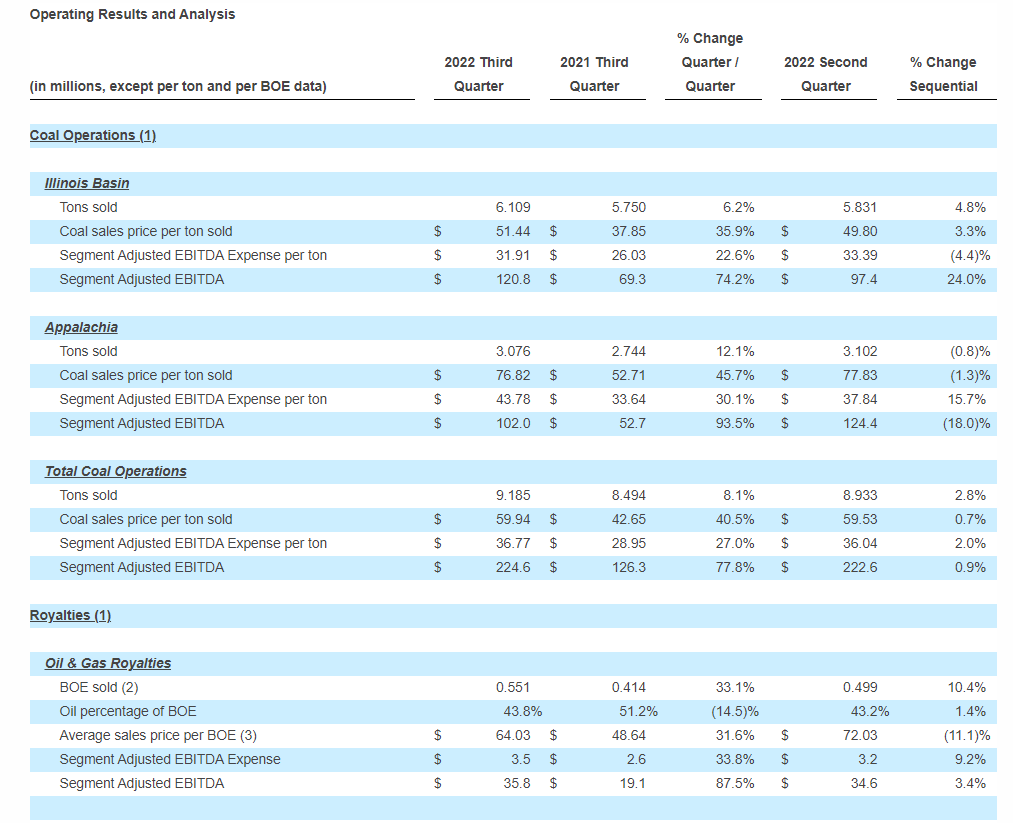

ARLP’s coal sales prices per ton increased significantly in both the Illinois Basin and Appalachia compared to the 2021 Quarter as improved price realizations in both the domestic and export markets drove coal sales prices higher by 35.9% and 45.7% in the Illinois Basin and Appalachia, respectively. Compared to the Sequential Quarter, coal sales price realizations improved as well. Increased domestic sales volumes drove coal sales volumes higher by 6.2% and 12.1% in the Illinois Basin and Appalachia, respectively, compared to the 2021 Quarter. Compared to the Sequential Quarter, Illinois Basin coal sales volumes increased 4.8% as a result of higher sales volumes at our Gibson South and Hamilton mines while coal sales volumes in Appalachia remained relatively consistent. ARLP ended the 2022 Quarter with total coal inventory of 1.4 million tons, representing an increase of 0.4 million tons compared to the end of the 2021 Quarter and a decrease of 0.2 million tons compared to the end of the Sequential Quarter.

Segment Adjusted EBITDA Expense per ton increased by 22.6% and 30.1% in the Illinois Basin and Appalachia, respectively, compared to the 2021 Quarter primarily as a result of ongoing inflationary pressures on numerous expense items, most notably labor-related expenses, supply and maintenance costs as well as increased sales-related expenses due to higher price realizations. Longwall moves at our Hamilton and Tunnel Ridge mines during the 2022 Quarter also contributed to higher per ton expenses compared to the 2021 Quarter. Compared to the Sequential Quarter, Segment Adjusted EBITDA Expense per ton in the Illinois Basin decreased 4.4% in the 2022 Quarter due to increased sales volumes, lower roof support expenses, higher recoveries at our Gibson South and Hamilton mines and a $6.5 million non-cash contingent accrual recorded in the Sequential Quarter related to our 2015 purchase of the Hamilton mine. These decreases were partially offset by an extended longwall move at our Hamilton mine during the 2022 Quarter. In Appalachia, Segment Adjusted EBITDA Expense per ton increased 15.7% compared to the Sequential Quarter as a result of adverse mining conditions and preparation plant maintenance improvements at MC Mining, higher labor-related expenses and supply costs as well as a longwall move at our Tunnel Ridge mine in the 2022 Quarter. These increases were partially offset by lower sales-related expenses due to decreased price realizations and increased recoveries at our Mettiki and Tunnel Ridge mines.

Our Oil & Gas Royalties segment had significantly higher volumes and sales price realizations per BOE in the 2022 Quarter which drove Segment Adjusted EBITDA higher by 87.5% to a record $35.8 million compared to $19.1 million for the 2021 Quarter. Compared to the Sequential Quarter, Segment Adjusted EBITDA increased by 3.4% in the 2022 Quarter primarily due to higher oil & gas volumes, which rose by 10.4%, partially offset by lower price realizations, which decreased by 11.1%.

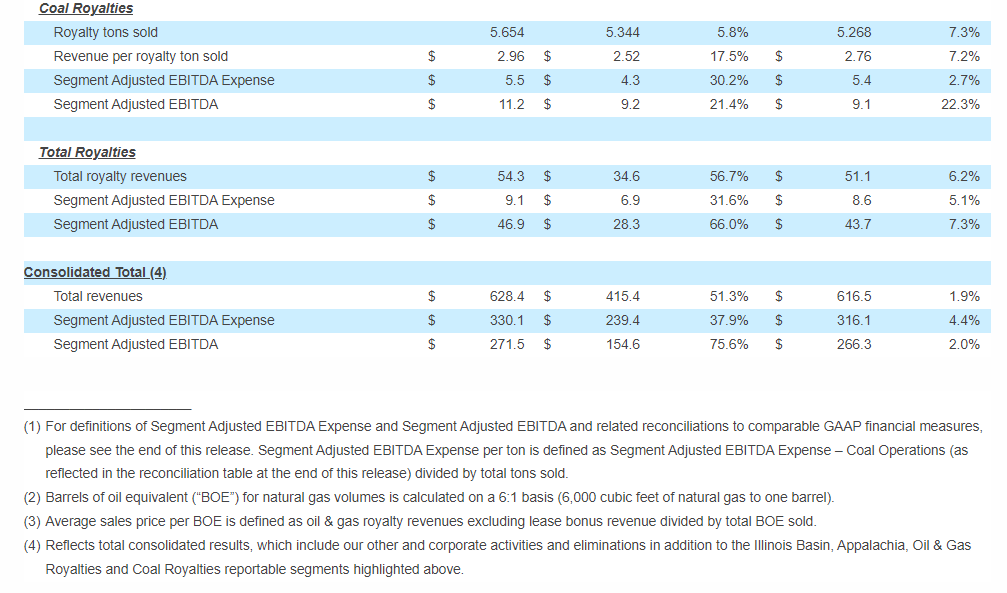

Segment Adjusted EBITDA for our Coal Royalties segment increased to $11.2 million, representing increases of 21.4% and 22.3% compared the 2021 and Sequential Quarters, respectively, as a result of increased royalty tons sold and higher average royalty rates per ton.

Outlook

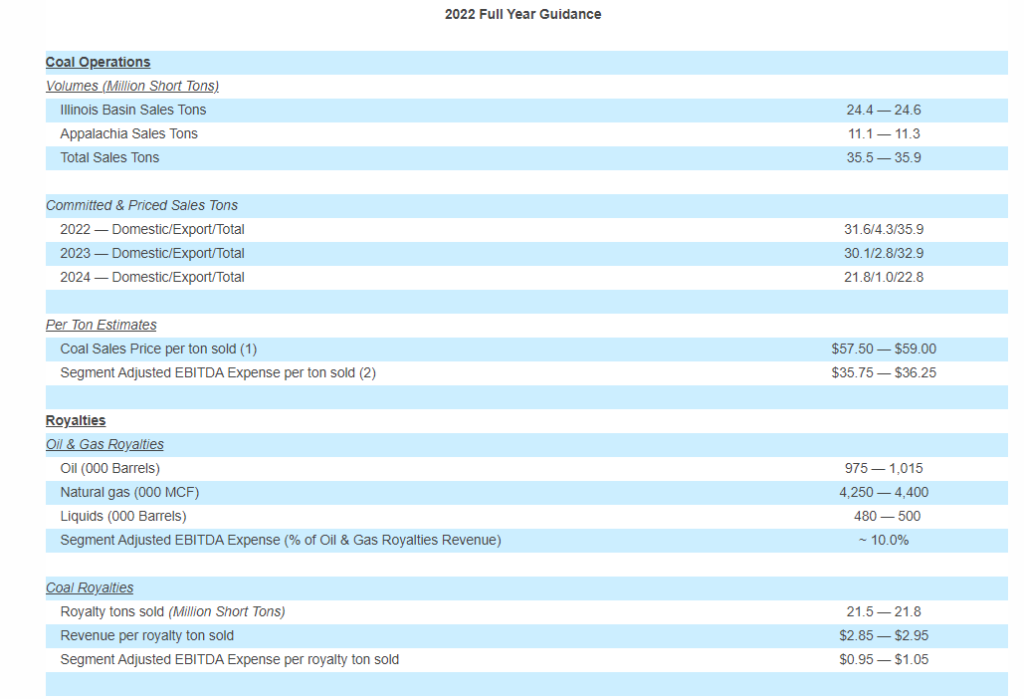

“Assisted by the supply driven energy crisis the world has experienced this year, ARLP is on track to achieve record financial results in 2022,” said Mr. Craft. “Since we have not seen a meaningful supply response, we expect the global energy markets will continue to be favorable for the foreseeable future. Based upon this view and our current contracted coal sales volumes, we expect to add up to two million tons of Illinois basin production next year giving us confidence our Partnership’s 2023 financial results will grow beyond this year’s record performance. In the near term, inflation pressures and continuing transportation challenges are the most significant issues our coal operations and marketing teams are managing. Rail performance has recently improved but low water levels and lock outages have impacted both exports destined for the U.S. Gulf and domestic barge traffic. These potential shipping delays may lead us to defer some of this year’s contracted tons into early next year. We have therefore adjusted our expectations for 2022 coal sales volumes, prices and costs as noted in the updated guidance table below. Our oil & gas royalties segment continues to benefit from increased drilling and completion activity by operators on our acreage and we have adjusted volume expectations accordingly.”

Mr. Craft continued, “Since our last earnings call in July, ARLP continued to invest for future growth. In keeping with our objective of reinvesting cash flows generated by our oil & gas royalty segment, we recently closed two transactions totaling $94.5 million to acquire an additional 4,322 net oil & gas royalty acres in the Permian Basin. There are currently 1,200 producing wells, 101 wells to be completed and 98 permitted locations on the acquired acreage, providing ARLP with line of sight to future oil & gas production growth. To enhance our long-lived, efficient mining operations and to maximize cash flow from our existing coal assets, we recently committed to access a resource area containing approximately 110 million tons adjacent to our River View mine allowing us to produce from a more productive, higher yield coal seam area and capture the opportunity to fully utilize existing infrastructure at this operation. In addition, during the 2022 Quarter, we added 69 million tons of lower cost, lower sulfur coal adjacent to our low-cost Tunnel Ridge longwall mine. We expect both of these investments will payout on cost savings alone and also give us the opportunity to add tons beyond 2024 to meet market demand, if available. Finally, ARLP recently elected to hold its commitment to Francis Energy at its initial $20 million convertible note investment. We remain interested in the EV infrastructure market and continue to evaluate opportunities in the industry to create value potential for ARLP.”

Mr. Craft concluded, “These are exciting times for ARLP. We believe our current core businesses are well positioned to deliver significant cash flows for some time to come, allowing ARLP to provide attractive cash returns to unitholders, effectively manage our balance sheet and invest in new opportunities to create long-term value for all of our stakeholders.”

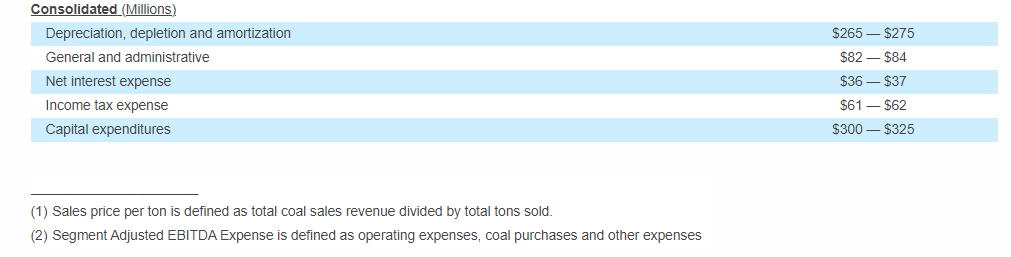

ARLP’s updated full year 2022 guidance is outlined below:

A conference call regarding ARLP’s 2022 Quarter financial results is scheduled for today at 10:00 a.m. Eastern. To participate in the conference call, dial (877) 407-0784 and request to be connected to the Alliance Resource Partners, L.P. earnings conference call. International callers should dial (201) 689-8560 and request to be connected to the same call. Investors may also listen to the call via the “investor relations” section of ARLP’s website at http://www.arlp.com.

An audio replay of the conference call will be available for approximately one week. To access the audio replay, dial U.S. Toll Free (844) 512-2921; International Toll (412) 317-6671 and request to be connected to replay using access code 13733069.

About Alliance Resource Partners, L.P.

ARLP is a diversified energy company that is currently the largest coal producer in the eastern United States. ARLP also generates operating and royalty income from mineral interests it owns in strategic coal and oil & gas producing regions in the United States. In addition, ARLP is positioning itself as an energy provider for the future by leveraging its core technology and operating competencies to make strategic investments in the fast-growing energy and infrastructure transition.

News, unit prices and additional information about ARLP, including filings with the Securities and Exchange Commission (“SEC”), are available at http://www.arlp.com. For more information, contact the investor relations department of ARLP at (918) 295-7674 or via e-mail at [email protected].

The statements and projections used throughout this release are based on current expectations. These statements and projections are forward-looking, and actual results may differ materially. These projections do not include the potential impact of any mergers, acquisitions or other business combinations that may occur after the date of this release. We have included more information below regarding business risks that could affect our results.

FORWARD-LOOKING STATEMENTS: With the exception of historical matters, any matters discussed in this press release are forward-looking statements that involve risks and uncertainties that could cause actual results to differ materially from projected results. Those forward-looking statements include expectations with respect to our future financial performance, coal and oil & gas consumption and expected future prices, our ability to increase unitholder distributions in future quarters, business plans and potential growth with respect to our energy and infrastructure transition investments, optimizing cash flows, reducing operating and capital expenditures, preserving liquidity and maintaining financial flexibility, among others. These risks to our ability to achieve these outcomes include, but are not limited to, the following: the outcome or escalation of current hostilities in Ukraine, the severity, magnitude, and duration of the COVID-19 pandemic and the emergence of new virus variants, including impacts of the pandemic and of businesses’ and governments’ responses to the pandemic, including actions to mitigate its impact and the development of treatments and vaccines, on our operations and personnel, and on demand for coal, oil, and natural gas, the financial condition of our customers and suppliers, available liquidity and capital sources and broader economic disruptions; changes in macroeconomic and market conditions and market volatility arising from hostilities in Ukraine, including inflation, changes in coal, oil, natural gas, and natural gas liquids prices, and the impact of such changes and volatility on our financial position; decline in the coal industry’s share of electricity generation, including as a result of environmental concerns related to coal mining and combustion and the cost and perceived benefits of other sources of electricity and fuels, such as oil & gas, nuclear energy, and renewable fuels; changes in global economic and geo-political conditions or in industries in which we or our customers operate; changes in coal prices and/or oil & gas prices, demand and availability which could affect our operating results and cash flows; actions of the major oil-producing countries with respect to oil production volumes and prices could have direct and indirect impacts over the near and long term on oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in competition in domestic and international coal markets and our ability to respond to such changes; potential shut-ins of production by operators of the properties in which we hold mineral interests due to low oil, natural gas, and natural gas liquid prices or the lack of downstream demand or storage capacity; risks associated with the expansion of our operations and properties; our ability to identify and complete acquisitions; our ability to identify and invest in new energy and infrastructure transition ventures; the success of our development plans for our wholly owned subsidiary, Matrix Design Group, LLC, and our investments in emerging infrastructure and technology companies; dependence on significant customer contracts, including renewing existing contracts upon expiration; adjustments made in price, volume, or terms to existing coal supply agreements; the effects of and changes in trade, monetary and fiscal policies and laws, including the interest rate policies of the Federal Reserve Board; the effects of and changes in taxes or tariffs and other trade measures adopted by the United States and foreign governments; legislation, regulations, and court decisions and interpretations thereof, both domestic and foreign, including those relating to the environment and the release of greenhouse gases, mining, miner health and safety, hydraulic fracturing, and health care; deregulation of the electric utility industry or the effects of any adverse change in the coal industry, electric utility industry, or general economic conditions; investors’ and other stakeholders’ increasing attention to environmental, social and governance matters; liquidity constraints, including those resulting from any future unavailability of financing; customer bankruptcies, cancellations or breaches to existing contracts, or other failures to perform; customer delays, failure to take coal under contracts or defaults in making payments; our productivity levels and margins earned on our coal sales; disruptions to oil & gas exploration and production operations at the properties in which we hold mineral interests; changes in equipment, raw material, service or labor costs or availability, including due to inflationary pressures; changes in our ability to recruit, hire and maintain labor, including as a result of the potential impact of government-imposed vaccine mandates; our ability to maintain satisfactory relations with our employees; increases in labor costs including costs of health insurance and taxes resulting from the Affordable Care Act, adverse changes in work rules, or cash payments or projections associated with workers’ compensation claims; increases in transportation costs and risk of transportation delays or interruptions; operational interruptions due to geologic, permitting, labor, weather, supply chain shortages of equipment or mine supplies, or other factors; risks associated with major mine-related accidents, mine fires, mine floods or other interruptions; results of litigation, including claims not yet asserted; foreign currency fluctuations that could adversely affect the competitiveness of our coal abroad; difficulty maintaining our surety bonds for mine reclamation as well as workers’ compensation and black lung benefits; difficulty in making accurate assumptions and projections regarding post-mine reclamation as well as pension, black lung benefits, and other post-retirement benefit liabilities; uncertainties in estimating and replacing our coal mineral reserves and resources; uncertainties in estimating and replacing our oil & gas reserves; uncertainties in the amount of oil & gas production due to the level of drilling and completion activity by the operators of our oil & gas properties; uncertainties in the future of the electric vehicle industry and the market for EV charging stations; the impact of current and potential changes to federal or state tax rules and regulations, including a loss or reduction of benefits from certain tax deductions and credits; difficulty obtaining commercial property insurance, and risks associated with our participation in the commercial insurance property program; evolving cybersecurity risks, such as those involving unauthorized access, denial-of-service attacks, malicious software, data privacy breaches by employees, insiders or others with authorized access, cyber or phishing-attacks, ransomware, malware, social engineering, physical breaches, or other actions; and difficulty in making accurate assumptions and projections regarding future revenues and costs associated with equity investments in companies we do not control.

Additional information concerning these and other factors can be found in ARLP’s public periodic filings with the SEC, including ARLP’s Annual Report on Form 10-K for the year ended December 31, 2021, filed on February 25, 2022 and amended on August 26, 2022, and ARLP’s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2022 and June 30, 2022, filed on May 9, 2022 and August 8, 2022, respectively. Except as required by applicable securities laws, ARLP does not intend to update its forward-looking statements.

Reconciliation of GAAP “net income attributable to ARLP” to non-GAAP “EBITDA” and “Distributable Cash Flow” (in thousands).

EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes and depreciation, depletion and amortization. Distributable cash flow (“DCF”) is defined as EBITDA excluding interest expense (before capitalized interest), interest income, income taxes and estimated maintenance capital expenditures. Distribution coverage ratio (“DCR”) is defined as DCF divided by distributions paid to partners.

Management believes that the presentation of such additional financial measures provides useful information to investors regarding our performance and results of operations because these measures, when used in conjunction with related GAAP financial measures, (i) provide additional information about our core operating performance and ability to generate and distribute cash flow, (ii) provide investors with the financial analytical framework upon which management bases financial, operational, compensation and planning decisions and (iii) present measurements that investors, rating agencies and debt holders have indicated are useful in assessing us and our results of operations.

EBITDA, DCF and DCR should not be considered as alternatives to net income attributable to ARLP, net income, income from operations, cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. EBITDA and DCF are not intended to represent cash flow and do not represent the measure of cash available for distribution. Our method of computing EBITDA, DCF and DCR may not be the same method used to compute similar measures reported by other companies, or EBITDA, DCF and DCR may be computed differently by us in different contexts (i.e. public reporting versus computation under financing agreements).

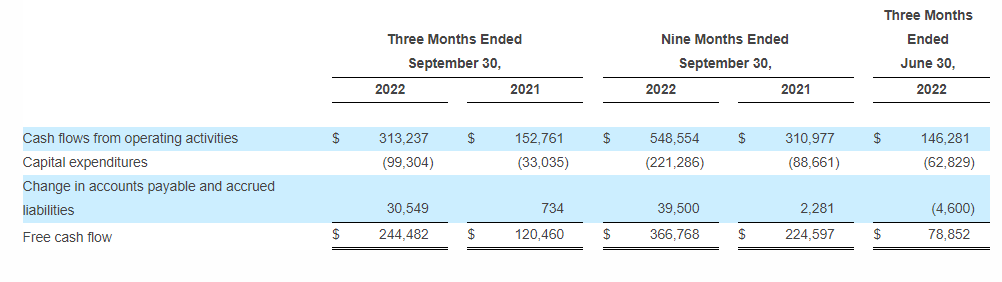

Reconciliation of GAAP “Cash flows from operating activities” to non-GAAP “Free cash flow” (in thousands).

Free cash flow is defined as cash flows from operating activities less capital expenditures and the change in accounts payable and accrued liabilities from purchases of property plant and equipment. Free cash flow should not be considered as an alternative to cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. Our method of computing free cash flow may not be the same method used by other companies. Free cash flow is a supplemental liquidity measure used by our management to assess our ability to generate excess cash flow from our operations.

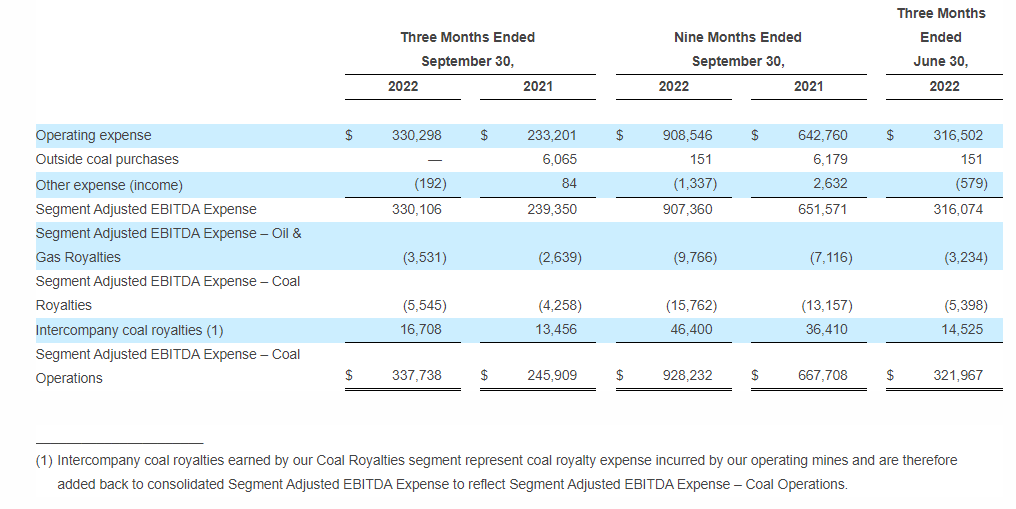

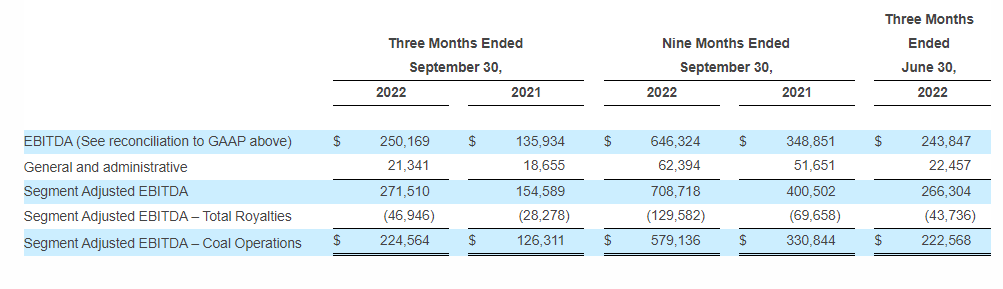

Reconciliation of GAAP “Operating Expenses” to non-GAAP “Segment Adjusted EBITDA Expense” and Reconciliation of non-GAAP ” EBITDA” to “Segment Adjusted EBITDA” (in thousands).

Segment Adjusted EBITDA Expense includes operating expenses, coal purchases and other expense. Transportation expenses are excluded as these expenses are passed through to our customers and, consequently, we do not realize any margin on transportation revenues. Segment Adjusted EBITDA Expense is used as a supplemental financial measure by our management to assess the operating performance of our segments. Segment Adjusted EBITDA Expense is a key component of EBITDA in addition to coal sales, royalty revenues and other revenues. The exclusion of corporate general and administrative expenses from Segment Adjusted EBITDA Expense allows management to focus solely on the evaluation of segment operating performance as it primarily relates to our operating expenses. Segment Adjusted EBITDA Expense – Coal Operations excludes expenses of our Oil & Gas Royalties segment and is adjusted for intercompany interactions with our Coal Royalties segment.

Segment Adjusted EBITDA is defined as net income attributable to ARLP before net interest expense, income taxes, depreciation, depletion and amortization and general and administrative expenses. Segment Adjusted EBITDA – Coal Operations excludes the contribution of our Oil & Gas and Coal Royalties segments to allow management to focus solely on the operating performance of our Illinois Basin and Appalachia segments.

Brian L. Cantrell

Alliance Resource Partners, L.P.

(918) 295-7673

Source: Alliance Resource Partners, L.P.