Wednesday, October 12, 2022

Michael Kupinski, Director of Research, Noble Capital Markets, Inc.

Patrick McCann, Research Associate, Noble Capital Markets, Inc.

Jacob Mutchler, Research Associate, Noble Capital Markets, Inc.

Refer to the bottom of the report for important disclosures

Overview: Developing A Shopping List. With the U.S. economy in the midst of a recession, we believe investors should be on the lookout for stocks on the “discount rack.” In our view, companies that possess ample funding and favorable growth characteristics could be well positioned to survive the downturn and be on the forefront of the subsequent economic recovery. This report highlights some of our favorite picks in the Entertainment & Leisure industries.

Entertainment: Bowlero Bowls Over Its Peers. Bowlero’s most recent fiscal quarter illustrated a continuation of the entertainment industry’s COVID rebound. Bowlero’s Group Event revenue grew 140% from the prior year period while total revenue was up 68%. With cash flow margins above 30% and cash on the balance sheet of $132 million, the company is poised to continue making accretive acquisitions in the fragmented bowling industry.

Gaming: Placing A Bet On Codere. The CDRO shares have been punished year-to-date (-58%) despite the company executing on its growth strategy as planned and maintaining pace to meet full-year guidance. Given a combination of robust growth in key Latin American markets and a balance sheet that boasts €84 million in cash and no LT debt, we believe the shares offer a favorable risk/reward relationship.

Esports: Motorsport Games Gets Funding. After a difficult second quarter a transformative restructuring plan has been implemented, which is estimated by the company to reduce overhead costs by 20% and save $4 million by the end of 2023. Additionally, Motorsport has secured $3 million from an existing credit line. These promising changes allow for more dollars to be spent on key revenue drivers.

Leisure. Travelzoo Readies A New Journey. Although Travelzoo (TZOO) is a digital media company, it is one of our favorite ways to play the recovering travel industry.

Investment Overview

Developing A Shopping List

The best time to buy stocks is typically in the midst of an economic recession. Investors begin to look beyond the economic weakness and begin positioning portfolios for an economic rebound. The hard part is determining when the economy is in the middle of the downturn. It appears by all standard definitions of an economic downturn that the U.S. is in an economic recession. But, how long will a downturn last? Should investors try to be cute to predict the midpoint of the downturn?

Many economic pundits paint the current state of the economy against the canvass of the 1970s, a period of high inflation and low economic growth. There are many similarities. The Federal Reserve in the early 70s was willing to provide cheap money to fuel the economy, without much concern about inflation. In the second half of the 70s, the economy was rocked by fuel supply shortages and high inflation. During the Covid pandemic, both fiscal and monetary policy was designed to provide liquidity and to make sure that people were able to pay their bills during the economic lockdowns. This had the affect of increasing personal income, even though GDP declined 31.4% in 2020. As the economy reopened, there was significant demand for goods and services, some of which were in short supply because of the previous and recurring economic lock downs. Simplistically, this fueled inflation, high demand with a consumer that had disposable income and limited supply.

As Figure #1 Early 1970s chart illustrates, the US economy grew 9.8%, as measured by real GDP, from January 1972 to September 1975. Notably, the stock market, as measured by the S&P 500 Index, declined a significant 18.6%. This was a period marked by rising inflation due to government spending. The inflation rate, as measured by the US Bureau of Labor Statistics, was a reasonable 3.3% in 1972, but increased to 11.1% in 1974 and then moderated slightly to 9.1% in 1975. The inflation rate remained above 5% for the following 3 years.

Figure #1 Early 1970s

Source: US Bureau of Economic Analysis and Yahoo Finance.

Given the current state of rising energy prices, many pundits paint the current US economic plight similar to the period of fuel shortages of the late 1970s. As Figure #2 Late 1970s illustrates, the US economy, as measured by real GDP, grew 13.5% from January 1977 to October 1981, an average of slightly more than 3% per year. Notably, inflation increased significantly, from 6.5% in 1977 to 11.3% in 1979, followed by 13.5% in 1980, and 10.3% in 1981. The stock market, as measured by the S&P 500 Index, did not react well, up 9.3% from January 1977 to October 1981, an average of 2.3% growth.

Figure #2 Late 1970s

Source: US Bureau of Economic Analysis and Yahoo Finance.

So, where are we now? In the present, the Covid induced government spending and stimulus related fiscal policy, large spending on the Ukraine war, and a Fed unwilling to reign in early signs of inflation has put the US in a dire economic position. Certainly, supply chain shortages contributed to the current rise in inflation, as well. The Fed now appears to have religion on inflation and is aggressively raising interest rates. The Fed indicated that it is willing to create economic pain to arrest inflationary pressures. Most certainly this will cause additional economic weakness. The stock market in the near to intermediate term will need to digest the likelihood of weakening corporate profits, as well. Furthermore, as it relates to the equity markets, other investment classes, such as bonds, may become more appealing, taking demand from the stock market.

We believe that arresting inflation would set a favorable trajectory for the stock market, as investors position for the prospect of an economic recovery. To some degree, the 24.4% drop in the stock market, as measured by the S&P 500 index, from January 2022 to near current levels, anticipate some of the headwinds for investors described earlier in this report, including weakening corporate profits, the prospect of a further weakened US, and, even global economy, a move toward other investment classes, and stubborn inflation. What is different this time is that the Fed now appears to be aggressively tackling inflation. As such, the 47% drop in the stock market from highs in 1973 to the low in 1974 may not be a prelude to the current environment. It was a different Fed and it took different actions.

We encourage a different approach than trying to time the market. Our advice is for investors to develop a shopping list and begin accumulating. But, be selective. We focus on companies with favorable balance sheets, or are well funded, have compelling growth characteristics, and attractive free cash flow. In other words, we look for companies that appear well positioned to come out on the other side of the recession and will benefit from an economic recovery.

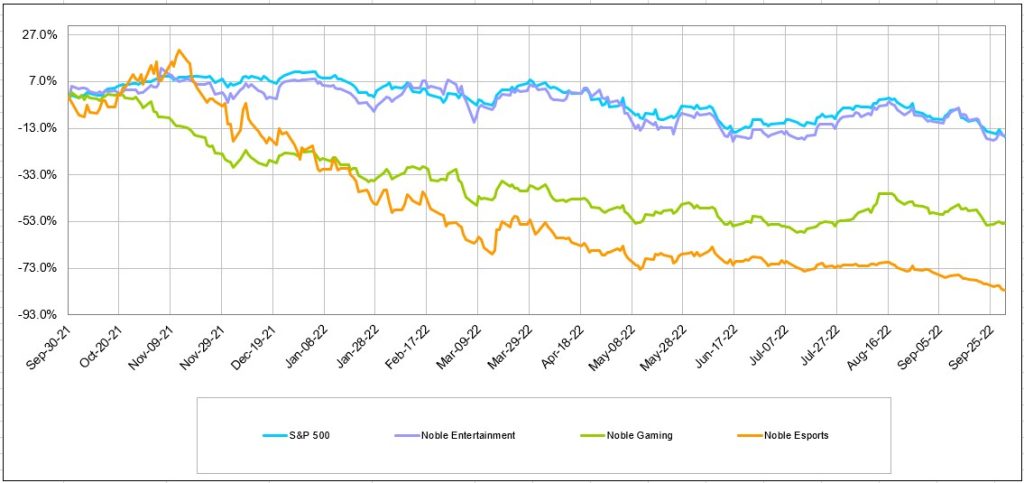

In this, our inaugural issue of the Entertainment and Leisure Industry Quarterly, we look at several companies that have favorable investment attributes for investors to consider. As Figure #3 Entertainment 12 Month Trailing Stock Performance Chart illustrates, the Entertainment Group performed poorly over the past 12 months. The Noble Entertainment index performed the best among our three Entertainment & Leisure sectors, down 16.1%, slightly outperforming the general market as measured by the S&P 500 Index, which decreased 16.8% in the comparable period. The Noble iGaming Index decreased 53.6% and the Noble eSports Index decreased 82.5% as these developmental industries were adversely affected by the closing of the capital markets to fund expansion. Given the weakness in these sectors, we look for the hidden gems. Some of our favorites highlighted in this report include: Bowlero (BOWL), Motorsport Games (MSGM), Travelzoo (TZOO) and Codere Online Luxemburg (CDRO)

Figure #3 Entertainment 12 Month Trailing Stock Performance

Source: Capital IQ

Entertainment Industry

Bowlero Bowls Over Its Peers

While the entertainment industry is broadly defined, we take a look at the Experiential Entertainment industry, in general, and at Bowlero (BOWL), specifically. In the latest quarter, the Noble Entertainment Index outperformed the general market, as measured by the S&P 500 Index, up 0.7% versus the general market decline of 5.3%. One of the contributors to the outperformance of the Entertainment group was Bowlero, up 16.2% in the comparable period.

The Bowlero shares reacted well to the company’s fiscal fourth quarter earnings release on September 15th. Q4 revenue of $267.7 million increased a strong 68% from year earlier levels and an impressive 42% above our estimate of $188.3 million. The strong revenue was attributed to favorable “walk-in” revenue, driven in part by a continuation of the Covid recovery. Adj. EBITDA was well above our estimate at $82.4 million, 45% higher than our forecast of $56.8 million.

How did Bowlero perform relative to its peers? As Figures #4 and #5 Entertainment Q2 Performance illustrates, Bowlero’s revenue growth for the comparable company peer second quarter outperformed its peers, save Live Nation. Live Nation’s revenue growth was 670%, reflecting the year earlier absence of events. Outside of Live Nation, Bowlero’s revenue growth of 68% compared favorably with the rest of its experiential entertainment peers, including Dave & Buster’s Entertainment’s, up 24%, and Vail Resorts, up roughly 31%.

Notably, management indicated that first quarter revenues are pacing 23% higher than year earlier results. As such, we raised our fiscal Q1 revenue forecast from $193.5 million to $222.5 million and raised our Q1 Adj. EBITDA estimate from $61.4 million to $72.0 million. Given strong operating momentum, we raised our fiscal full year 2023 revenue estimate to $983.5 million from $899.3 million and our Adj. EBITDA estimate to $322.2 million from $301.3 million. While we anticipate Bowlero’s revenue growth will slow as it faces more difficult comps due to the post Covid recovery and potential economic weakness, we believe that the company is well positioned. Furthermore, we expect that the company will grow revenues faster than most of its peers post Covid recovery due to the growth potential of its industry.

Figure #4 Entertainment Q2 Performance

Source: Company 10Qs

Figure #5 Entertainment Q2 Performance

Source: Company 10Qs

As of July 3, the company had $132.2 million in cash and $865.1 million in long-term debt. Debt is a comfortable 2.6 times our calendar year 2023 adj. EBITDA estimate, with net debt a conservative 2.1 times. With a large cash balance and strong cash flow generation (32% adj. EBITDA margin), we believe the company is well positioned to repurchase stock, upgrade its facilities, and/or acquire new facilities. The company has a large $200 million share repurchase authorization, of which it repurchased 3.3 million shares at an average share price of $10.07. There is a large repurchase authorization remaining. Furthermore, we believe that the company will seek acquisition fueled growth, possibly in other experiential center based facilities other than bowling.

Notably, the BOWL shares trade at 8.6 times our revised calendar full year 2023 adj. EBITDA forecast, below peers which currently trade near 9.5 times. Figure #6 Entertainment Comparables highlight the stock valuations in the experiential entertainment group. Given its favorable growth profile, (the company has grown faster than its peers), a healthy balance sheet, compelling stock valuation, and prospects for acquisition fueled growth, we view the Bowlero shares as among our favorites in the sector and one to put on a shopping list for a recovery play.

Figure #6 Entertainment Comparables

Source: Capital IQ and Noble estimates.

iGaming Industry

Placing A Bet On Codere

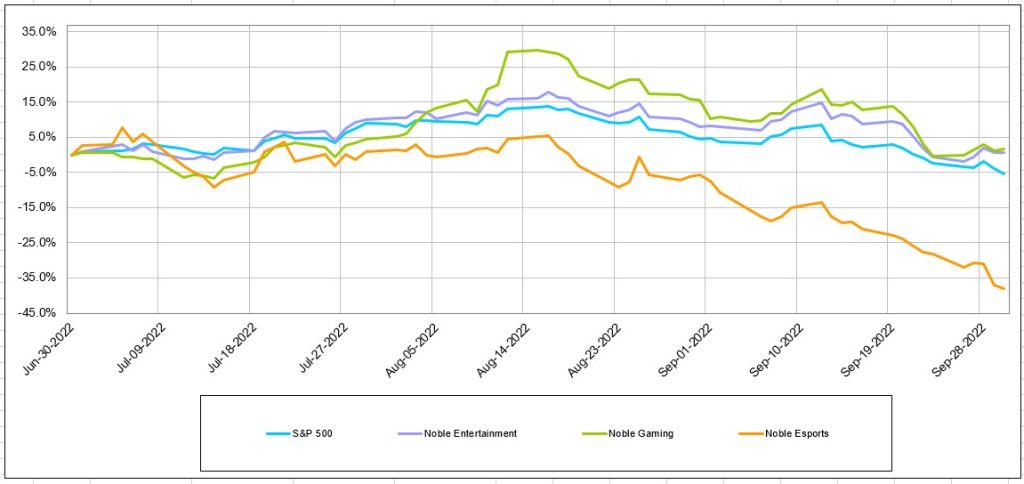

The past year has been tough on the iGaming industry. The Noble iGaming Index is down nearly 54% versus a negative 17% for the general market, as measured by the S&P 500 Index. In the latest quarter, the iGaming stocks seemed to have stabilized, up 1.6% versus a continued general market decline, down 5.3% for the general market. Interestingly, as Figure #7 Third Quarter Stock Performance chart illustrates, the iGaming sector was the best performing sector among the Entertainment and Esports sectors, which were up a modest 0.7% and down 38.1%, respectively.

The shares of Codere Online Luxembourg could not fight the headwinds of the industry wide selling pressure. The CDRO shares dropped 70% from its post de-SPACing in December 2021 to near current levels. The weakness in the shares has been in spite of the company executing on its growth strategy as planned and maintaining its fundamental pace to meet full-year guidance. In the latest quarter, the shares drifted 3.9% versus the industry which increased 1.6%.

Figure #7 Third Quarter Stock Performance

Source: Capital IQ

We believe that the CDRO shares are a victim of throwing the baby out with the bath water. The poor performance of the iGaming industry in many respects is due to the developmental nature of the industry. Many of the companies included in the Noble iGaming index do not generate positive cash flow. As such, balance sheets have been supporting growth investment. Certainly, there will be a shake-out of players in the industry that do not have the financial capability to invest for growth. We believe that Codere Online is one of the survivors.

First, the company has been executing on its development plans to expand its operations in Latin America, as evidenced by favorable quarterly results. The latest second quarter net gaming revenue grew 41% to $29.2 million, accelerating from the 24% year-over-year growth in Q1. At $11.9 million, Mexico accounted for nearly 41% of the revenue, growing 85% over the prior year period. Operations in Columbia contributed $2.2 million, with 56% growth. Even revenue in Spain grew 12%, despite restrictions on marketing in the country.

Given a combination of robust growth in key Latin American markets and a balance sheet that boasts €84 million in cash and no LT debt, we believe the shares offer a favorable risk/reward relationship. We believe the company is off to a good start since the completion of the SPAC merger, with strong execution of its growth strategy in Latin America. Management is continuing expansion with plans to add to the company’s presence in Argentina. In August, the company completed its application for an online gambling license in Cordoba, Argentina’s second-most populous province. If the company is granted a license, which would likely happen before year-end, it would begin operations shortly after the issuance. Notably, Cordoba will issue up to 10 licenses and Codere Online is one of just 10 applicants. Management believes there is an opportunity for the company to be a market leader in Argentina. To that end, the company expanded its partnership with Argentine soccer club River Plate, during the quarter becoming the club’s primary sponsor. The Codere logo is now on the front of the club’s jersey, which will increase the company’s visibility in the country.

Although the company is not yet cash flow positive, its operations in Spain generated its highest quarterly cash flow since Q2 2020. Adj. EBITDA in Spain was $3.6 million, enough to offset 87% of the $4.1 million adj. EBITDA loss from the company’s operations in Mexico. Interestingly, the marketing restrictions in the country came with a silver lining of lower competition. This is because the restrictions make it harder for newer operators to establish their brands in the country. Additionally, the lower marketing costs contributed to the strong cash flow generation. Notably, management expects similar cash flow generation going forward for the Spanish operations. We view the situation in Spain favorably as the consistent cash flow profile will help fund the expansion in Latin America and have a mitigating impact on the company’s cash burn.

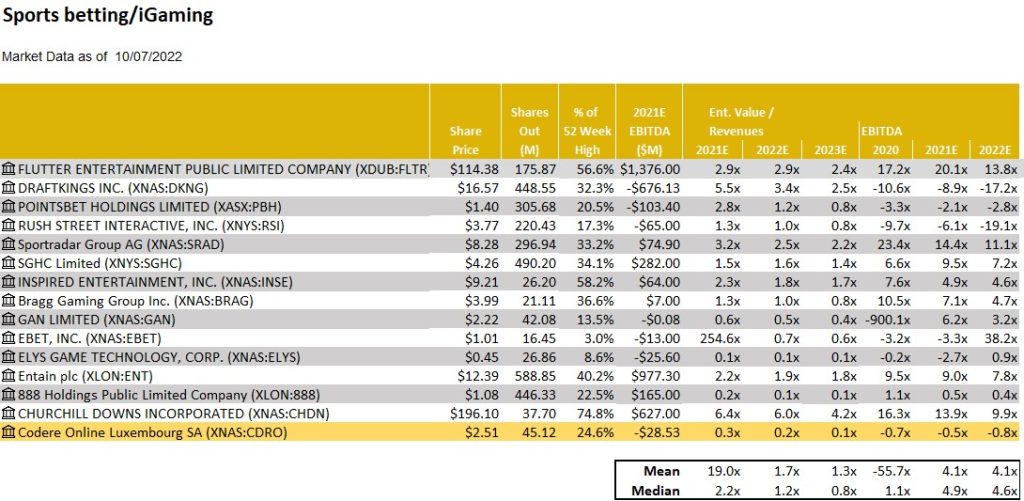

Figure #8 iGaming Comparables highlight the stock valuations in the iGaming industry and the valuation gap between the industry and Codere. Near current levels, the CDRO shares trade at 0.2 times enterprise value to 2023 expected revenue. Like other companies that have negative cash flow, the CDRO shares have suffered in recent months. However, Codere Online does not appear to be in need of funding to execute on its growth strategy. As such, we believe that investors have not differentiated it from its peers. Our price target of $9 reflects a target EV/2023 revenue multiple of 2 times, more in line with peers of 4 times, but with additional headroom for upside. The shares are rated Outperform.

Figure #8 iGaming Comparables

Source: Capital IQ and Noble estimates.

Esports Industry

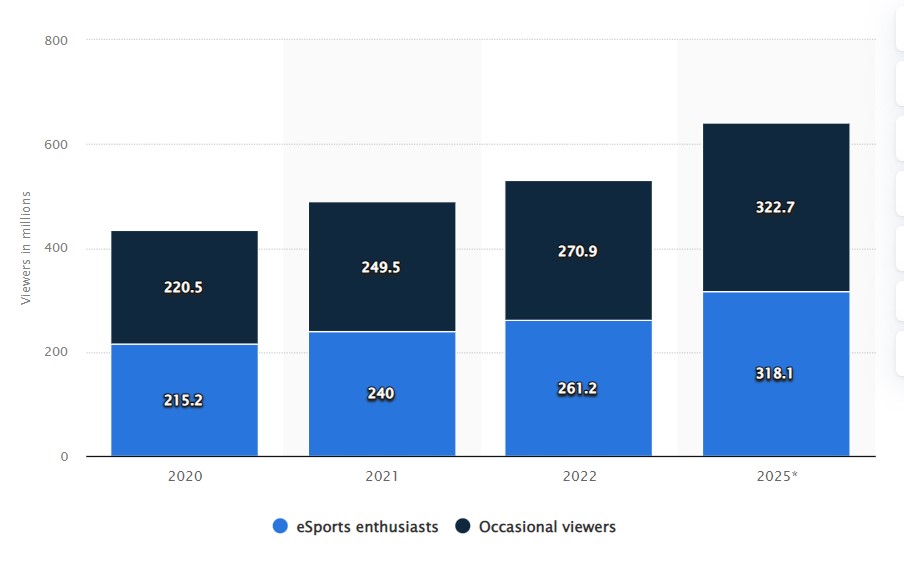

The Esports industry had a difficult year and a difficult quarter in terms of stock performance. The horrible stock performance does not reflect the overall industry trends. Video gaming is still on the rise. It is estimated that there are 2.7 billion gamers worldwide, expected to achieve an estimated 3.0 billion gamers in 2023, based on Newzoo’s numbers. The video game market is expected to reach $159.3 billion this year and grow to $200.0 billion in 2023. So, what about the Esports industry? Esports viewership was elevated during the Covid lockdowns, with viewership significantly higher. As Figure #9 Esports Viewership Outlook illustrates, viewership trends are expected to increase even from the elevated 2020 levels to over 640 million viewers in 2025.

In spite of the compelling industry fundamental trends, the individual esports companies in the space are struggling. Many of the companies were developmental, and, as such, were caught without investment spend as the capital markets closed. We find some gems in the rubble of the esports industry. The stock that we would like to highlight in this report is Motorsport Games (MSGM). Motorsport Games is a publisher of motorsport video games, with the rights to iconic racing games such as NASCAR and 24 Hour of LeMans. After a high of $15.50 in October 2021, the shares are currently trading at $0.78 per share.

Recently, the company announced several moves to shore up its financing until it releases a set of new motorsport games in 2023. At that time, the company is expected to significantly improve its financial capability to invest in future updates to its expanding game portfolio. First, the company announced that it will decrease overhead by an annualized $4 million. Secondly, the company will receive a $3 million cash advance from its majority shareholder, Motorsport Network. This agreement is under the same terms as its previous $12 million line of credit, which had been paid off. Finally, the company plans to have a 1 for 10 reverse stock split. This move is to maintain NASDAQ listing requirements.

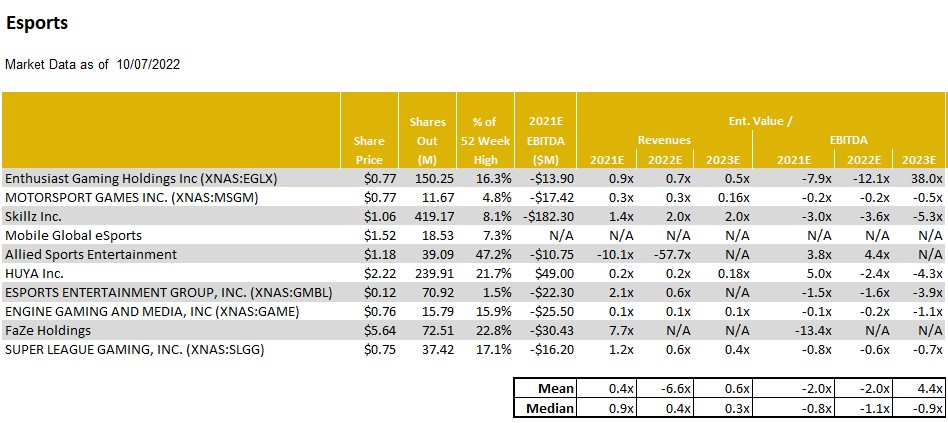

Near current levels, the MSGM shares trade at an enterprise value below cash value, well below peers as Figure #10 Esports Comparables illustrate. We view the shares as an option on the company’s ability to fund its operations long enough to launch its new titles and cash in on its world class licensing agreements. We view the shares as a high risk/high reward opportunity, suitable only for speculative investors. We rate the shares Outperform with a price target of $2.50. Notably, our price target, which represents significant upside, implies a conservative target enterprise value of just 0.7 times 2023 revenue. Please read the attached report for important disclosures.

Figure #9 Esports Viewership Outlook

Source: Newzoo/Statista

Figure #10 Esports Comparables

Source: Capital IQ and Noble estimates.

Leisure Industry

The Leisure industry is a very broad industry. In this report, we highlight a company that is in the Travel Leisure industry, but is really an advertising/media company. But, because its business is closely aligned with the travel industry, we have included it in this Leisure report. The company is Travelzoo. Much like the travel industry, there has been fits and starts with the recovery post Covid. Many countries are now open, travel restrictions are gone, and, even Covid/mask policies have relaxed. But, the industry, in general, and Travelzoo, in particular, are dealing with the weakening global economies.

In the recent second quarter, the favorable revenue momentum from the first quarter fizzled. Total company revenues declined 7.3% year over year and were down roughly 4% from the first quarter. Some seasonality appears to be at play here. The question will be whether the softness in the quarter was related to general macro economic trends and if those trends appear to be evident heading into the third quarter. We believe that the weak quarter is related to choppiness in revenue due to the company’s transition toward advertising rather than “getaway” voucher sales. As such, we do not believe that there is an unraveling of the fundamental underpinning of the company.

The company sold travel “getaway” vouchers during the Covid pandemic. Those voucher sales accounted for as much as 60% of total company revenues. Now that the travel industry is coming back, the company has pivoted toward its traditional advertising focused model. We estimate that “getaway” voucher sales were between 15% to 20% of total revenues in the latest quarter. Given that advertising represents a higher margin business, gross margins were higher than expected in the quarter (87.8% versus our 85.4% estimate). But, advertising was not as strong as what we had hoped. Management believes that travel demand increased beyond the capability of the travel industry. While prices increased for airline tickets, the industry was not able to deal with the demand given staffing shortages. Similarly, hotels faced the same issue. As a result, airlines have cutback on flights. More recently, given a waning consumer demand and softening US economy, airline prices are coming back down. We believe that the company is entering a more favorable environment given softening demand. In other words, the travel industry will need to provide favorable deals to lure consumers to travel. That is the sweet spot for Travelzoo.

Notably, the company has a flexible and improving balance sheet. As of June 30, the company had $26.6 million in cash and restricted cash and no long term debt. The company had $47.9 million in merchant liabilities (which reflects the amount of un-redeemed voucher sales). The amount of cash would be expected to be reduced as vouchers are redeemed. There are roughly $14 million in receivables. Management indicated that credit card receivables collection should significantly enhance its cash position in 2023. Given that the company will be generating positive cash flow, it is possible that the company will begin share repurchases. The company has a 1 million share repurchase authorization. The company did not repurchase shares in the latest quarter.

Near current levels, the shares trade at just 4.6 times enterprise value to our 2023 adj. EBITDA estimate, using a fully-diluted share count of 14.9 million. Our price target of $10, reflects a target multiple of 8.3 times enterprise value to our 2023 adj. EBITDA estimate. We believe over the next quarter or two revenue growth acceleration could serve as a catalyst to drive the share price higher. The shares are rated Outperform. Please see the report for important disclosures and information.

The latest report on the companies mentioned in this report may be downloaded by clicking on the respective company name:

GENERAL DISCLAIMERS

All statements or opinions contained herein that include the words “we”, “us”, or “our” are solely the responsibility of Noble Capital Markets, Inc.(“Noble”) and do not necessarily reflect statements or opinions expressed by any person or party affiliated with the company mentioned in this report. Any opinions expressed herein are subject to change without notice. All information provided herein is based on public and non-public information believed to be accurate and reliable, but is not necessarily complete and cannot be guaranteed. No judgment is hereby expressed or should be implied as to the suitability of any security described herein for any specific investor or any specific investment portfolio. The decision to undertake any investment regarding the security mentioned herein should be made by each reader of this publication based on its own appraisal of the implications and risks of such decision.

This publication is intended for information purposes only and shall not constitute an offer to buy/sell or the solicitation of an offer to buy/sell any security mentioned in this report, nor shall there be any sale of the security herein in any state or domicile in which said offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such state or domicile. This publication and all information, comments, statements or opinions contained or expressed herein are applicable only as of the date of this publication and subject to change without prior notice. Past performance is not indicative of future results. Noble accepts no liability for loss arising from the use of the material in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to Noble. This report is not to be relied upon as a substitute for the exercising of independent judgement. Noble may have published, and may in the future publish, other research reports that are inconsistent with, and reach different conclusions from, the information provided in this report. Noble is under no obligation to bring to the attention of any recipient of this report, any past or future reports. Investors should only consider this report as single factor in making an investment decision.

IMPORTANT DISCLOSURES

This publication is confidential for the information of the addressee only and may not be reproduced in whole or in part, copies circulated, or discussed to another party, without the written consent of Noble Capital Markets, Inc. (“Noble”). Noble seeks to update its research as appropriate, but may be unable to do so based upon various regulatory constraints. Research reports are not published at regular intervals; publication times and dates are based upon the analyst’s judgement. Noble professionals including traders, salespeople and investment bankers may provide written or oral market commentary, or discuss trading strategies to Noble clients and the Noble proprietary trading desk that reflect opinions that are contrary to the opinions expressed in this research report.

The majority of companies that Noble follows are emerging growth companies. Securities in these companies involve a higher degree of risk and more volatility than the securities of more established companies. The securities discussed in Noble research reports may not be suitable for some investors and as such, investors must take extra care and make their own determination of the appropriateness of an investment based upon risk tolerance, investment objectives and financial status.

Company Specific Disclosures

The following disclosures relate to relationships between Noble and the company (the “Company”) covered by the Noble Research Division and referred to in this research report.

Noble is not a market maker in any of the companies mentioned in this report. Noble intends to seek compensation for investment banking services and non-investment banking services (securities and non-securities related) with any or all of the companies mentioned in this report within the next 3 months

ANALYST CREDENTIALS, PROFESSIONAL DESIGNATIONS, AND EXPERIENCE

Senior Equity Analyst focusing on Basic Materials & Mining. 20 years of experience in equity research. BA in Business Administration from Westminster College. MBA with a Finance concentration from the University of Missouri. MA in International Affairs from Washington University in St. Louis.

Named WSJ ‘Best on the Street’ Analyst and Forbes/StarMine’s “Best Brokerage Analyst.”

FINRA licenses 7, 24, 63, 87

WARNING

This report is intended to provide general securities advice, and does not purport to make any recommendation that any securities transaction is appropriate for any recipient particular investment objectives, financial situation or particular needs. Prior to making any investment decision, recipients should assess, or seek advice from their advisors, on whether any relevant part of this report is appropriate to their individual circumstances. If a recipient was referred to Noble Capital Markets, Inc. by an investment advisor, that advisor may receive a benefit in respect of

transactions effected on the recipients behalf, details of which will be available on request in regard to a transaction that involves a personalized securities recommendation. Additional risks associated with the security mentioned in this report that might impede achievement of the target can be found in its initial report issued by Noble Capital Markets, Inc.. This report may not be reproduced, distributed or published for any purpose unless authorized by Noble Capital Markets, Inc..

RESEARCH ANALYST CERTIFICATION

Independence Of View

All views expressed in this report accurately reflect my personal views about the subject securities or issuers.

Receipt of Compensation

No part of my compensation was, is, or will be directly or indirectly related to any specific recommendations or views expressed in the public

appearance and/or research report.

Ownership and Material Conflicts of Interest

Neither I nor anybody in my household has a financial interest in the securities of the subject company or any other company mentioned in this report.